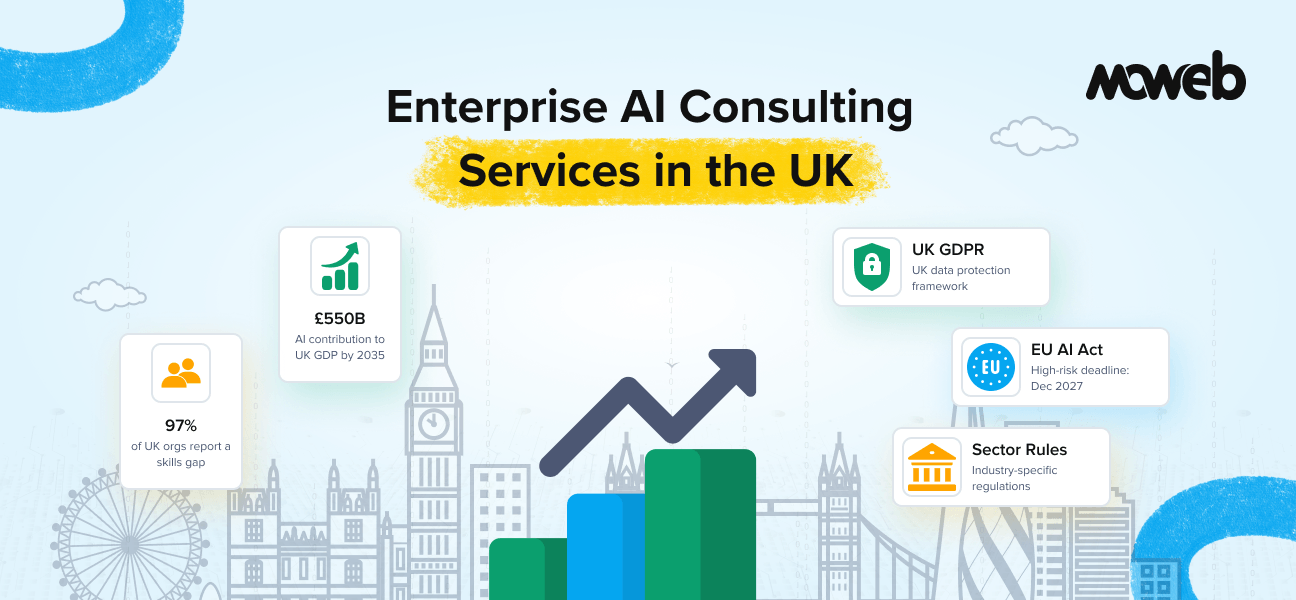

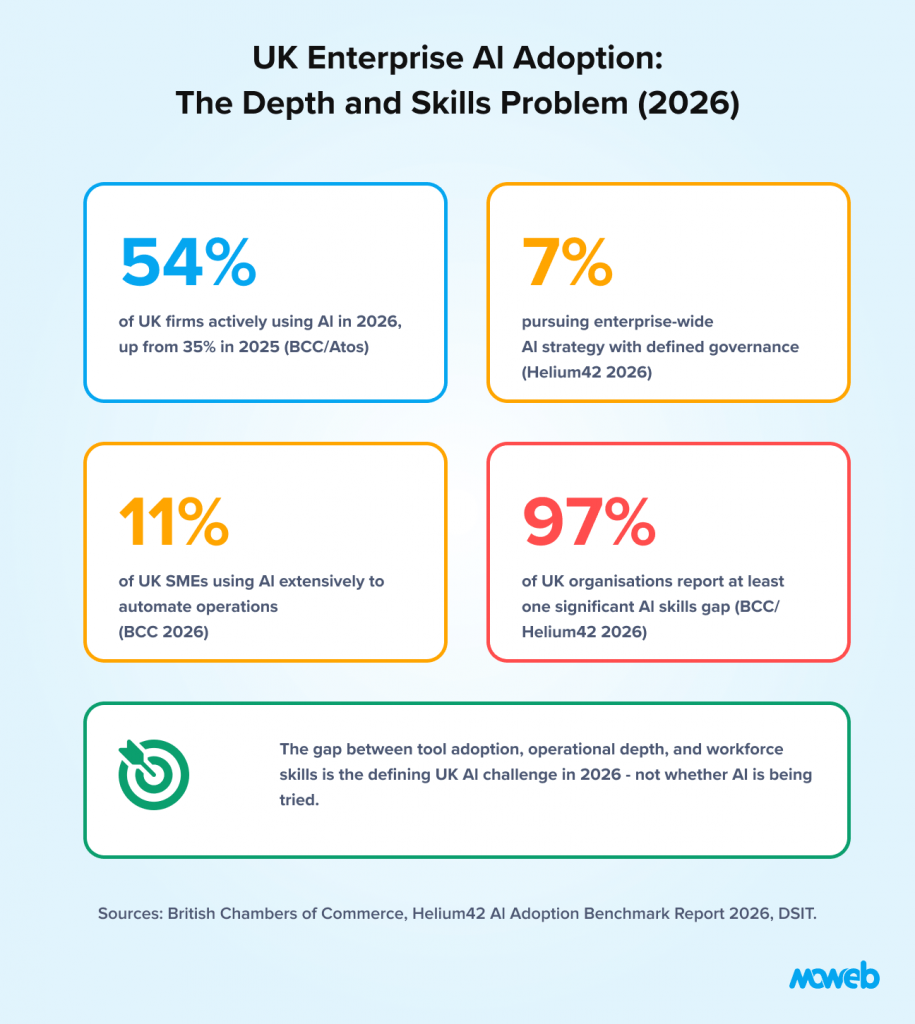

What is the current state of enterprise AI adoption in the UK? 54% of UK firms are actively using AI in 2026, up from 35% in 2025 and 25% in 2024, according to the British Chambers of Commerce. However, depth of adoption varies enormously. Only 7% of UK organisations are pursuing an enterprise-wide AI strategy with defined governance. Only 11% of UK SMEs use AI extensively to automate or streamline operations. Most UK businesses are at surface level a Microsoft Copilot licence or ChatGPT subscription without structured workflows, training, or governance behind it. A separate and arguably more urgent finding from the BCC’s 2026 workforce report: 97% of UK organisations report at least one significant AI skills gap, and just 14% of UK workers have received any formal AI training. The gap between tool adoption and operational value is not primarily a technology problem it is a skills and governance problem. AI could contribute £550 billion to UK GDP by 2035, but capturing that value requires moving from tool adoption to systemic deployment.

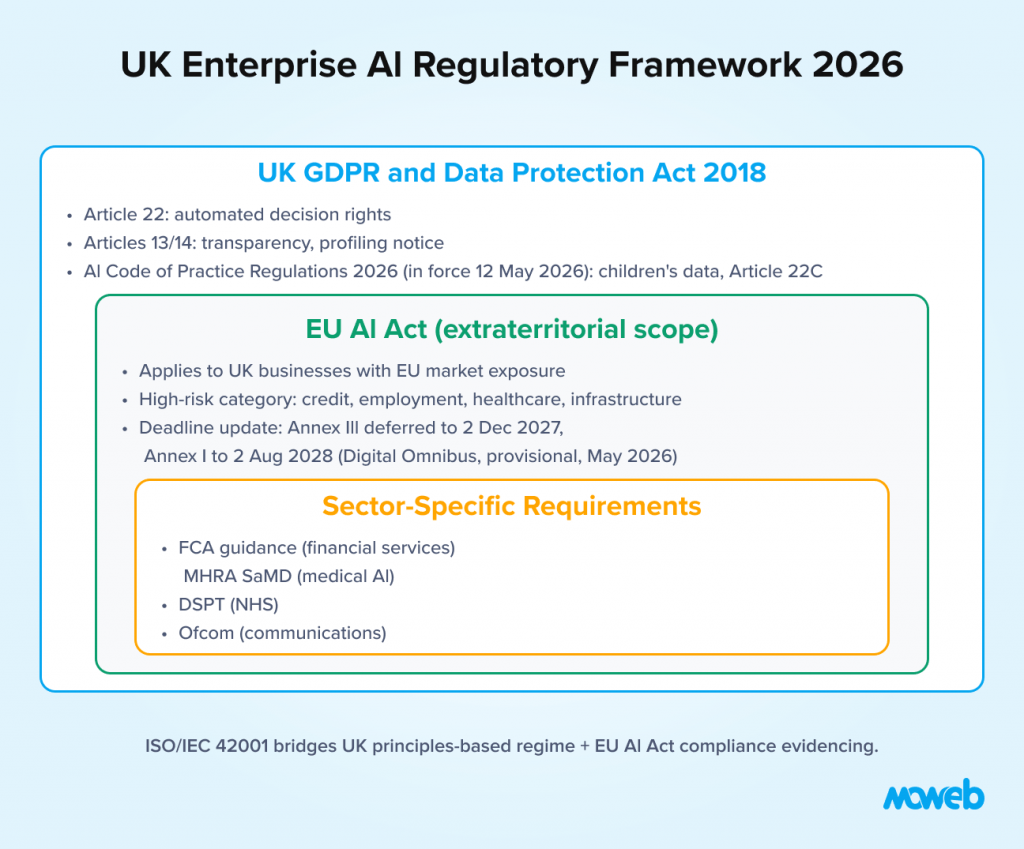

What regulatory framework applies to AI in UK businesses? UK businesses face a layered regulatory framework for AI. UK GDPR and the Data Protection Act 2018 govern how personal data is used in AI systems – with specific implications for automated decision-making under Articles 13-22. The EU AI Act applies to any UK business with EU market operations or EU customer relationships – its high-risk category requirements for automated decision-making in credit, employment, and healthcare contexts apply regardless of the deploying organisation’s location. Note that the EU AI Act’s high-risk system deadline, originally set for 2 August 2026, was provisionally deferred to 2 December 2027 for Annex III systems (and 2 August 2028 for product-embedded systems) under the EU’s Digital Omnibus agreement of 7 May 2026 though this remains pending formal adoption at time of writing, and the underlying obligations are unchanged, only the timeline. FCA guidance on AI in financial services applies to UK financial institutions, and a new UK-specific instrument the AI Code of Practice Regulations 2026 (SI 2026/425), in force from 12 May 2026 requires the Information Commissioner to prepare a code of practice on AI and automated decision-making, including specific provisions on children’s data. The UK’s own AI regulatory approach (principles-based, sector-specific) is less prescriptive than the EU framework but is tightening in regulated sectors.

The United Kingdom is the third-largest AI market in the world, behind only the United States and China. AI investment in UK startups grew 80% in 2025, accounting for a third of all UK venture capital deployed. The UK Government’s own projections put AI’s potential contribution to UK GDP at £550 billion by 2035.

Against this backdrop, the actual state of UK enterprise AI adoption is revealing. According to the British Chambers of Commerce, 54% of UK firms are now actively using AI – up sharply from 35% in 2025. But the depth data tells a different story. Only 7% of UK organisations are pursuing an enterprise-wide AI strategy with defined governance. Only 11% of UK SMEs use AI extensively to automate operations. The majority have a Copilot licence or a ChatGPT account – but not an AI programme.

The skills picture, when examined closely, is starker still. The BCC’s 2026 workforce research, conducted with Helium42, found that 97% of UK organisations have at least one significant AI skills gap, with 28% saying this is already hurting their ability to meet business objectives. Just 14% of UK workers have undertaken any formal AI training, and EY’s research puts the figure receiving genuinely adequate training at 11%. Perhaps most striking: UK firms that have used AI for at least a year reported net job losses of 8% over the previous 12 months the highest rate among major economies and roughly double the international average, though it is worth noting that 95% of SMEs using AI report no impact on workforce size, suggesting the job loss effect is concentrated in a minority of deeper, bespoke deployments rather than typical Copilot-level usage.

The gap between the ambition of the UK AI market and the operational reality of most UK enterprises is not a technology problem. The UK Government’s own AI Adoption Research found that 60% of businesses cited limited AI skills and expertise as the key blocker, while 71% had not identified a clear use for AI in their organisation. The constraint is strategic and organisational, not technical.

This is precisely the context in which enterprise AI consulting services add the most value: helping UK businesses move from tool adoption to systemic operational deployment, within a regulatory environment that is increasingly specific and a competitive landscape where the window to establish advantage is open but will not stay open indefinitely.

This guide covers what UK businesses need to understand about enterprise AI consulting in 2026: the UK-specific regulatory context, the sectors leading adoption and why, what to look for in an AI consulting partner, and how to structure an engagement that generates real operational value rather than another underutilised pilot.

The UK AI Regulatory Landscape: What Businesses Need to Know

The regulatory context for AI in the UK differs from both the EU and the US in ways that directly affect how AI systems must be designed, governed, and deployed. Understanding this landscape before engaging an AI consulting partner is essential for UK businesses in regulated sectors.

UK GDPR and the Data Protection Act 2018 are the foundational data governance frameworks for any AI system that processes personal data in the UK. Three provisions have specific AI implications.

Article 22 of the UK GDPR restricts automated decision-making that has a significant legal or similarly significant effect on individuals. If an AI system makes or substantially influences decisions about credit, employment, insurance, or similar outcomes, individuals have the right not to be subject to solely automated decisions, the right to request human review, and the right to an explanation. This right-to-explanation requirement shapes which AI architectures are permissible for regulated decisions and directly impacts model design.

Articles 13 and 14 require that individuals are informed when their data is used for automated processing and profiling. This has implications for AI systems that build individual profiles – customer segmentation, credit scoring, HR screening tools – where individuals interact with the system without necessarily knowing their data is being processed. A recent UK-specific development worth noting: the AI Code of Practice Regulations 2026 (SI 2026/425), in force since 12 May 2026, specifically requires the Information Commissioner to prepare guidance on AI and automated decision-making with particular provisions for children’s data under the newly introduced Article 22C of UK GDPR.

Data minimisation principles under UK GDPR require that AI training datasets use only the minimum personal data necessary for the defined purpose, with documented justification for any personal data included. Training a customer service AI on unredacted personal customer communications requires a legal basis and documented necessity assessment.

The EU AI Act applies to UK businesses in ways that are frequently misunderstood. Post-Brexit, the EU AI Act does not directly regulate UK operations as a matter of UK law. However, it applies to any AI system that is placed on the EU market or whose outputs are used by EU-based individuals or organisations. A UK financial services firm using an AI system to make decisions about EU customers, or a UK manufacturer deploying AI systems sold into EU markets, is within scope of the EU AI Act’s obligations even though the deploying organisation is UK-based.

The high-risk category under the EU AI Act covering AI used in credit, employment decisions, essential services, education, critical infrastructure, and law enforcement carries the most demanding obligations: conformity assessment, technical documentation, human oversight mechanisms, EU database registration, and post-market surveillance. Important timing update: the original 2 August 2026 deadline for these obligations has been provisionally deferred under the EU’s Digital Omnibus package, agreed in principle on 7 May 2026. Annex III high-risk systems (recruitment, credit scoring, law enforcement, education, essential services) now have until 2 December 2027 to comply; Annex I systems embedded in regulated products (medical devices, machinery) have until 2 August 2028. This deferral is provisional; it has political agreement but is pending formal adoption and publication in the EU Official Journal, and the underlying technical requirements have not changed, only the compliance timeline. UK businesses with EU market exposure should treat the extended timeline as the current planning baseline while continuing compliance preparation, since the obligations themselves remain exactly as demanding as before.

FCA guidance on AI in financial services is the most developed UK sector-specific AI regulatory framework in 2026. The FCA’s Consumer Duty, its guidance on model risk management, and its increasingly specific expectations around AI transparency, fairness testing, and governance documentation set requirements that go substantially beyond general data protection obligations. Financial services firms deploying AI in customer-facing or decision-influencing applications need AI consulting partners with genuine FCA regulatory understanding, not just general AI competence.

The UK’s principles-based AI approach – which the government has signalled will remain less prescriptive than the EU framework creates flexibility for UK businesses but also creates ambiguity. In the absence of prescriptive rules, the risk management responsibility sits more squarely with the deploying organisation. This makes internal AI governance frameworks more important, not less, for UK enterprises in the current regulatory environment. ISO/IEC 42001, the international AI Management System standard, has emerged as the practical bridge between the UK’s principles-based regime and the EU AI Act’s more prescriptive requirements, a single governance framework that evidences compliance posture for both regulatory environments simultaneously. For the full AI governance framework that UK regulatory compliance requires, see our guide to AI governance for LLMs and enterprise agents.

UK Sector AI Adoption: Where the Activity Is and Why

AI adoption in the UK is not uniform across sectors. Understanding where adoption is leading and where it is lagging helps UK businesses calibrate their competitive urgency.

Financial services leads UK enterprise AI adoption by deployment depth and investment level. Sector-specific 2026 benchmark data puts financial services strategic adoption at 21–31%, the clear leader alongside information and communications (43–51%) and ahead of professional services (20–28%). The sector’s data richness, its tolerance for technology investment, and the FCA’s active engagement with AI governance are combining to accelerate adoption. AI applications leading deployment include: fraud detection and AML transaction monitoring, credit risk assessment and underwriting automation, regulatory compliance monitoring, customer service automation, and algorithmic trading and risk management. The FCA’s openness to regulatory dialogue around AI through its TechSprint events and Innovation Pathways programme means that well-governed AI deployments in financial services can receive regulatory clarity that reduces deployment risk. For the specific AI use cases generating the clearest ROI in UK financial services, see our guide to AI in fintech: fraud detection, underwriting, and compliance automation.

Legal services is the sector with the highest AI investment growth rate in 2026 relative to its prior AI adoption level. The document-intensive nature of legal work – contract review, due diligence, regulatory research, litigation support – is highly amenable to AI automation. Approximately 40% of UK law firms had experimented with generative AI for drafting by late 2025, with investment accelerating in 2026. The primary applications are contract intelligence (clause extraction, risk flagging, obligation tracking), legal research assistance, and document generation for standard transaction types.

Healthcare and the NHS present the highest-value and most regulatory-complex AI opportunity in the UK. NHS AI adoption faces the dual challenge of DSPT (Data Security and Protection Toolkit) compliance requirements and MHRA Software as a Medical Device regulations for clinical AI, alongside persistent budget and procurement constraints in NHS trusts. Private healthcare and pharmaceutical research have moved more quickly. The ICB (Integrated Care Board) structure has created new procurement pathways for AI that work more efficiently than traditional NHS trust-level procurement. For the healthcare AI use cases most relevant to UK NHS and private healthcare contexts, see our guide to AI in healthcare operations.

Manufacturing and industrial is where AI ROI is most directly quantifiable and where UK adoption is lagging relative to UK manufacturing’s competitive importance. UK 2026 benchmark data places manufacturing-adjacent sectors well behind the leaders: construction strategic adoption sits at roughly 6%, among the lowest of any UK sector despite clear use cases in planning, safety, and predictive maintenance, and German and Scandinavian manufacturers remain ahead of the UK on industrial AI deployment more broadly. UK manufacturers investing in predictive maintenance, quality inspection, and energy optimisation AI are building competitive advantages that are difficult to replicate quickly once established.

Professional services and consulting – accounting, advisory, HR services, management consulting have seen rapid deployment of AI productivity tools at the individual level (Copilot, ChatGPT) but slow deployment of AI systems at the operational level. This sector sits in the 20–28% strategic adoption band per 2026 UK benchmark data, ahead of retail, healthcare, and hospitality (11–15%) but behind financial services and information/communications. The sector’s fragmented client data and variable document standards make systematic AI deployment more complex than in industries with more standardised data environments.

The Five UK-Specific Considerations When Engaging an AI Consulting Partner

UK businesses evaluating AI consulting partners need to apply the general evaluation criteria covered in our guide to how to choose an enterprise AI development company, plus five considerations specific to the UK context.

1. UK regulatory fluency, not just general compliance awareness An AI consulting partner claiming regulatory competence for UK financial services should be able to articulate the specific FCA guidance on model risk, Consumer Duty implications for AI systems, and the distinction between UK GDPR Article 22 and EU GDPR Article 22 post-Brexit. A partner who responds to “what are our UK GDPR obligations under Article 22 for this credit assessment AI?” with “we comply with GDPR” has not demonstrated UK-specific regulatory fluency. It demonstrates generic compliance awareness. The difference matters for UK regulated deployments.

2. EU AI Act scope assessment for UK businesses with EU exposure Many UK businesses incorrectly assume the EU AI Act does not apply to them because they are UK-domiciled. An AI consulting partner serving UK businesses with EU market exposure should proactively assess EU AI Act scope as part of the discovery process — identifying whether the proposed AI system falls within scope and what obligations apply, and on what timeline, given the Digital Omnibus deferral discussed above. This is not a standard capability of all AI consulting firms. It is a differentiator for firms with genuine cross-jurisdictional regulatory knowledge.

3. Integration with UK enterprise systems UK enterprises have specific system configurations that differ from US market defaults. Microsoft 365 and Azure are dominant in UK enterprise, with Salesforce and SAP common in larger enterprises. Legacy systems vary – UK financial services has a significant proportion of mainframe and bespoke platform infrastructure. UK public sector and NHS organisations use procurement frameworks (Crown Commercial Service, NHS Shared Business Services) that affect how AI consulting engagements are structured and procured. A consulting partner with genuine UK enterprise delivery experience will understand these specifics rather than encountering them as surprises mid-engagement.

4. IR35 and contractor structure implications UK businesses engaging AI consulting firms that use contractor teams should understand IR35 implications for off-payroll working. Some AI consulting firms structure their delivery teams as contractors that may have IR35 implications for the UK client depending on the engagement model. This is not a reason to avoid consulting firms that use contractors – it is a reason to understand the contracting structure before signing and to ensure appropriate IR35 assessments have been completed.

5. Time zone and communication alignment: For UK businesses working with AI consulting firms headquartered outside the UK, time zone alignment matters more than it might initially appear. BST (British Summer Time, UTC+1) and GMT (UTC) create a 5.5-hour gap with India and no gap with continental Europe. For AI development engagements where daily stand-ups, architecture reviews, and rapid decision-making are required, the communication model should be explicitly agreed – not left to assumption. Firms with genuine UK presence or structured overlap windows are significantly easier to work with than those that operate primarily in non-overlapping time zones.

What UK Enterprise AI Consulting Engagements Actually Look Like

The structure of a credible AI consulting engagement for a UK enterprise follows the same four-phase structure described in detail in our guide to enterprise AI consulting services: what to expect from an engagement. What differs in the UK context is the content of specific phases.

Discovery phase for UK businesses should include: a UK GDPR and Data Protection Act assessment of the proposed data flows and processing activities, a preliminary EU AI Act scope assessment for businesses with EU market exposure, an assessment of any sector-specific regulatory requirements (FCA, CQC, MHRA, Ofcom), and an honest assessment of where the organisation’s data infrastructure sits relative to what the proposed AI system requires.

The discovery phase should NOT be a scoping call followed immediately by a proposal. UK businesses with significant regulatory exposure – financial services, healthcare, legal services – need a genuine 2-3 week discovery phase that includes appropriate technical and regulatory assessment before a proposal can be meaningful.

Development phase for UK businesses should produce not just a working AI system but the governance documentation required for UK regulatory environments: a Data Protection Impact Assessment (DPIA) for any processing of personal data, technical documentation sufficient to respond to a regulatory examination or an Article 22 explanation request, and access control documentation aligned with UK GDPR minimum necessary principles.

Knowledge transfer for UK businesses should include briefing of the data protection officer or in-house legal counsel (if applicable) on the system’s data flows, processing activities, and compliance architecture – not just technical team training. Compliance-aware knowledge transfer is a UK-specific delivery requirement that standard engagement templates from US-market firms often overlook.

The UK AI Skills Gap: Why It Shapes AI Consulting Demand

The most important structural driver of AI consulting demand in the UK market is not AI enthusiasm or competitive pressure. It is the skills gap.

60% of UK businesses cited limited AI skills and expertise as the key blocker to AI adoption. The scale of the gap is wider than that single statistic suggests. The BCC’s 2026 workforce research found 97% of UK organisations report at least one significant AI skills gap, with only 35% of UK business leaders running a mature, organisation-wide AI upskilling programme and just 11% of UK employees receiving training that EY’s research would classify as genuinely adequate. This is not a market dynamic that resolves quickly: training AI practitioners takes years, hiring them is competitive against US and EU employers with larger compensation budgets, and retaining them in non-technology UK industries is a persistent challenge.

For UK businesses outside the technology sector, the practical implication is that internal AI capability is unlikely to be sufficient for production AI deployment in the near to medium term. AI consulting firms that transfer knowledge to internal teams – rather than creating dependency relationships – are significantly more valuable to UK businesses navigating this skills gap than those that maximise ongoing service revenue by maintaining exclusive ownership of the system knowledge.

The knowledge transfer dimension of any AI consulting engagement is more commercially important for UK businesses than for their US counterparts, simply because the UK talent market makes post-engagement internal capability more difficult to build. A consulting firm that commits explicitly to knowledge transfer – documented architecture, operational runbooks, team training, and defined independence at engagement end – is not just a better partner commercially. It is the only sustainable model for a UK enterprise that cannot rely on internal AI talent to maintain what the consultant built.

How to Get Started: A Practical First Step for UK Businesses

The most common mistake UK businesses make when starting an AI programme is attempting to start everywhere simultaneously – multiple tool evaluations, multiple pilot projects, and multiple vendor conversations running in parallel without a clear framework for deciding what to build first.

A structured AI readiness assessment – covering data quality, infrastructure maturity, use case clarity, and governance readiness – is the most productive first step. Our AI readiness assessment checklist for mid-sized enterprises provides the framework for conducting this assessment internally, identifying the specific gaps that need addressing before an AI consulting engagement will deliver production value.

For UK businesses unsure where to start across their enterprise AI programme, the starting point that consistently generates the clearest ROI with the lowest governance complexity is an internal knowledge assistant built on RAG – as covered in our guide to what is the best first AI use case for finance, ops, and support teams. It operates on existing internal documents, generates immediate employee productivity benefits, and establishes the data infrastructure and governance discipline that more ambitious AI deployments require.

Frequently Asked Questions About Enterprise AI Consulting in the UK

Does the EU AI Act apply to UK businesses? Yes, in specific circumstances. The EU AI Act applies to any AI system placed on the EU market or whose outputs are used by EU-based individuals or organisations regardless of where the deploying organisation is based. UK businesses that sell products containing AI components into EU markets, provide services to EU customers, or have EU subsidiaries are within scope for relevant provisions. The high-risk category requirements covering AI used in credit, employment, healthcare, education, and critical infrastructure are the most demanding. Note that the compliance deadline for these requirements has shifted: the original 2 August 2026 date was provisionally deferred under the EU’s May 2026 Digital Omnibus agreement to 2 December 2027 for most high-risk (Annex III) systems, and 2 August 2028 for product-embedded (Annex I) systems. This deferral has political agreement but is pending formal adoption; the underlying obligations are unchanged, only the timeline has moved.

What is the UK GDPR Article 22 right and how does it affect AI systems? Article 22 of the UK GDPR gives individuals the right not to be subject to solely automated decisions that have a significant legal or similarly significant effect on them. For enterprises, this means: AI systems that make or substantially influence credit, employment, insurance, or similar decisions must have human review available on request; the logic of the decision must be explainable in meaningful terms; and purely automated decision-making in these contexts requires specific legal bases. This provision directly affects which AI architectures are permissible for regulated decision-making in UK deployments.

What certifications should UK businesses require from an AI consulting partner? ISO 27001:2022 is the standard security management certification. ISO/IEC 42001:2023, the international AI Management System standard, is increasingly the practical bridge for evidencing governance against both the UK’s principles-based regime and the EU AI Act simultaneously worth requiring or asking about directly. For UK financial services clients: evidence of FCA regulatory understanding. For healthcare: understanding of DSPT requirements and MHRA SaMD framework. CMMI Level 3 compliance signals process maturity. For UK public sector procurement: consideration of G-Cloud framework registration and relevant Crown Commercial Service supplier status. UK-specific regulatory knowledge is more important than the certifications themselves; certifications should be the floor, not the ceiling of the evaluation.

How does AI consulting for UK SMEs differ from enterprise engagements? UK SMEs face budget constraints that make full-scale consulting engagements less accessible than for large enterprises. The most effective approach for UK SMEs is a focused, time-boxed assessment and first deployment – typically 8-12 weeks for a single use case – rather than an open-ended programme engagement. Prioritise use cases where the data is already clean and accessible (internal documents, existing CRM records) and where the ROI is immediately visible. The first AI deployment should be sized to prove value quickly and generate executive confidence for subsequent investment.

Is the UK Government providing support for AI adoption? Yes, through several programmes. Innovate UK provides grant funding for AI research and development projects. The AI Opportunity Fund and various sector-specific programmes (NHS AI Lab, Catapult networks) provide targeted support for healthcare and industrial AI. Made Smarter offers manufacturing AI adoption support in certain regions. The AI Safety Institute (now AISI) publishes guidance on responsible AI development that informs governance best practice. UK businesses exploring AI investments should assess whether any programmes apply to their sector and scale before committing full programme budgets.

What is the typical cost of enterprise AI consulting in the UK market? UK market pricing for specialist AI consulting firms typically runs £120-250 per hour or £60,000-£180,000 for a first production deployment engagement. Global consultancies (Accenture, Deloitte, KPMG, PwC) operate at £250-500 per hour with minimum engagements of £400,000 or more. For UK mid-market enterprises, specialist firms that combine advisory capability with engineering execution at the £120-250 per hour range offer the best value proposition. As with US engagements, total cost of ownership over 12 months – including ongoing infrastructure, support, and knowledge transfer investment – should be modelled before engaging.

What is the UK AI skills gap and how does it affect AI consulting engagements? The UK AI skills gap is substantial: 97% of UK organisations report at least one significant AI skills gap (BCC/Helium42, 2026), only 35% of UK business leaders run a mature organisation-wide AI upskilling programme, and just 11–14% of UK employees have received adequate or any formal AI training. For AI consulting engagements, this means knowledge transfer is not a nice-to-have but a commercial necessity; UK businesses are less likely than US counterparts to have the internal capability to maintain a system after a consulting engagement closes without an explicit, well-documented transfer of architecture knowledge, operational runbooks, and team training.

Conclusion: The UK AI Window Is Open – But Execution Depth Is What Will Determine Winners

The UK AI market in 2026 has a fundamental tension at its centre. The headline adoption numbers are strong and improving. The depth of that adoption – governance, operational integration, skills capability – is lagging far behind. The businesses that close this gap in the next 12-18 months will be the ones with a structural competitive advantage as AI capabilities continue to compound.

AI consulting for UK businesses in 2026 is less about helping businesses understand what AI can do – most UK leaders understand the opportunity – and more about helping them execute correctly within a UK regulatory environment that demands governance-by-design, a UK skills market that limits internal capability, and a competitive landscape where the gap between AI leaders and laggards is widening.

The 7% of UK businesses with enterprise-wide AI strategy and defined governance are not more technologically sophisticated than the other 93%. They made a different organisational decision: to treat AI as a programme requiring structured investment, governance design, and measured expansion rather than as a technology experiment. With 97% of UK organisations reporting at least one significant skills gap, that decision now extends explicitly to how knowledge is transferred and retained, not just how the AI system is built. That decision, made now, is worth considerably more than the same decision made in 18 months.

Moweb works with UK enterprises, professional services firms, and technology companies to design and deliver AI programmes that perform in production – with UK regulatory context built into every engagement from discovery through to knowledge transfer. Our AI Strategy & Consulting and Generative AI & LLM development practices serve UK clients with the same governance discipline and production-oriented delivery model we bring to US and India market engagements. Talk to us about your UK AI programme.

Found this post insightful? Don’t forget to share it with your network!